For decades, banks have been the cornerstone of borrowing and lending. If you needed a mortgage, a business loan, or even just a credit card, the local bank was your gateway. But in the last few years, something remarkable has happened: blockchain technology has given birth to decentralized finance (DeFi). Suddenly, people are lending and borrowing without traditional banks at all. This shift begs an important question: could DeFi actually replace banks in the lending industry?

The Rise of Blockchain Lending

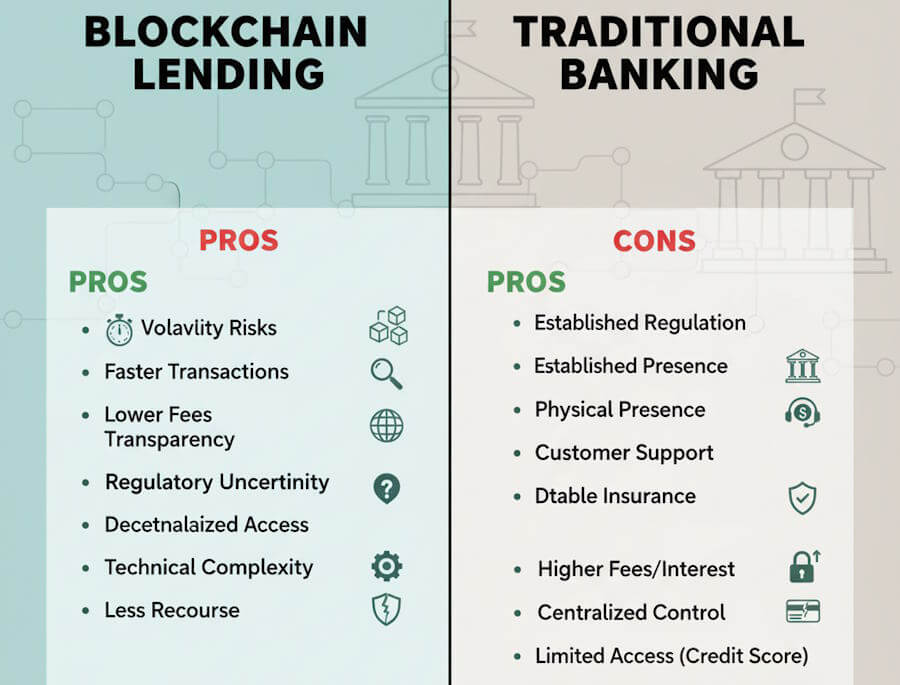

Blockchain is essentially a decentralized ledger—transparent, immutable, and not controlled by a single authority. When applied to lending, it enables peer-to-peer transactions without intermediaries. DeFi platforms like Aave, Compound, and MakerDAO allow users to lock up their crypto assets and borrow against them instantly. Instead of waiting for a bank’s approval, smart contracts automatically enforce the rules of the loan.

Why People Are Drawn to DeFi

Traditional lending often comes with slow approval processes, strict requirements, and hidden fees. DeFi, on the other hand, offers speed, transparency, and global access.

A user in Kenya can borrow from a lender in Canada without either of them stepping into a bank branch. This opens up financial opportunities for millions who are unbanked or underbanked.

At the same time, people are becoming more aware of how their borrowing behaviors affect their financial standing. For instance, many borrowers wonder how Affirm can impact your credit score and compare that experience to what decentralized platforms offer, where credit scores are often irrelevant. Instead of relying on FICO or Experian, DeFi lending relies on collateral locked in smart contracts.

Challenges That DeFi Faces

Despite its promise, decentralized lending is not without hurdles. Smart contracts can contain bugs, and once deployed, they are difficult to change. Hacks and exploits have already cost DeFi users billions. Moreover, crypto markets are notoriously volatile—collateral values can drop overnight, leading to sudden liquidations.

There’s also the regulatory angle. Governments worldwide are still figuring out how to treat DeFi. Should it be taxed like securities? Should lending protocols require Know Your Customer (KYC) checks? Without clear guidelines, both lenders and borrowers face uncertainty.

Comparing Traditional Banks and DeFi Platforms

To better understand whether DeFi could truly replace banks, let’s compare the two models side by side:

| Aspect | Traditional Banks | DeFi Platforms |

|---|---|---|

| Approval Process | Lengthy, requires credit checks and documentation | Instant via smart contracts, no credit checks |

| Accessibility | Limited by geography and banking infrastructure | Global, anyone with internet and crypto wallet |

| Transparency | Opaque; terms and fees often buried in fine print | Fully transparent; rules coded into smart contracts |

| Risks | Regulated and insured, but slower and costly | Unregulated, vulnerable to hacks and volatility |

Will DeFi Replace Banks, or Just Transform Them?

It’s tempting to imagine a future where DeFi completely eliminates banks. But the reality might be more nuanced. Banks are already experimenting with blockchain technology to streamline their own processes. Some may even adopt hybrid models where they use DeFi-like mechanisms under a regulated umbrella.

Consider the early days of the internet: many people thought newspapers and TV would vanish completely. Instead, traditional media adapted to the digital world. Similarly, banks might adapt by incorporating DeFi tools while maintaining regulatory safeguards.

The Human Element of Borrowing

Lending is not just about money—it’s about trust and relationships. Many people still find comfort in knowing there’s a person or institution to call if something goes wrong. DeFi can feel intimidating and impersonal, especially for those not deeply immersed in crypto. Until user experiences improve, many borrowers may still prefer traditional banks despite the inefficiencies.

Conclusion

DeFi has cracked open the doors to a radically different lending system—one that is faster, borderless, and decentralized. Yet, it’s unlikely to fully replace banks in the near future. Instead, we may see a blended future where DeFi protocols coexist with traditional banking, each serving different needs. Banks provide stability and regulation; DeFi delivers speed and innovation.

The question isn’t so much “Will DeFi replace banks?” but rather “How will both evolve together?” In the end, the borrower wins by gaining more options, more flexibility, and more power in shaping their financial journey.